Strategies Explained

Written By Ehsaan XP

Last updated 7 months ago

Understanding different strategies is crucial to making informed decisions about how you manage your AI Basket. In this chapter, we'll explore two primary approaches:

The BUY & HOLD Strategy

The Rebalancing Strategy

We'll also discuss Dollar Cost Averaging as an adjustment to the BUY & HOLD strategy. We'll define each, delve into how allocation works within them, discuss their pros and cons, and help you determine which might be the best fit for your goals.

The BUY & HOLD Strategy

Definition and Basic Principles

The BUY & HOLD strategy is one of the simplest and most common approaches. It involves purchasing a set of assets and holding onto them for an extended period, regardless of market fluctuations. The idea is to benefit from the long-term appreciation of the assets over time.

How Allocation Works in BUY & HOLD

Choosing Initial Allocation:

Selecting Assets: You begin by choosing the assets you want to include in your basket. This could be based on factors like personal interest, market research, or selecting a predefined basket on the platform.

Setting Allocation Percentages: Decide how much of your total investment to allocate to each asset. For example, you might allocate 50% to Asset A and 50% to Asset B, or distribute your funds across multiple assets in varying proportions.

Factors to Consider:

Risk Tolerance: Allocate more to assets you consider stable if you prefer lower risk.

Growth Potential: Allocate more to assets you believe have higher growth potential.

Diversification: Spread your allocation to reduce exposure to any single asset.

How Allocation Changes Over Time:

Market Movements: As the market values of your assets change, the proportion of your total basket that each asset represents will also change.

Example:

Initial Allocation: 50% Asset A, 50% Asset B.

After Market Movement: Asset A increases in value and now represents 60% of your basket, while Asset B represents 40%.

Impact on Your Basket:

Increased Risk Exposure: Assets that grow significantly can come to dominate your basket, increasing your exposure to their specific risks.

Unintended Allocation Drift: Over time, your basket may no longer reflect your initial strategy or risk profile due to these shifts.

Managing Allocation Changes:

Passive Approach: In BUY & HOLD, you typically accept these changes and do not make adjustments.

Awareness: It's important to be aware of how your allocation is shifting, even if you choose not to act on it.

Pros and Cons

Pros

Simplicity: Easy to implement without the need for constant monitoring or adjustments.

Lower Transaction Costs: Fewer trades mean reduced fees and commissions.

Potential for Significant Gains: If the assets appreciate significantly over time, you could see substantial returns.

Avoids Market Timing: Eliminates the stress of trying to predict short-term market movements.

Cons

Lack of Risk Management: Allocation shifts can lead to increased risk if certain assets decline significantly.

Missed Opportunities: You might miss out on gains from reallocating funds to better-performing assets.

Overexposure: Assets that grow significantly can dominate your basket, potentially increasing risk.

Emotional Challenges: Holding onto assets during market downturns can be psychologically difficult.

Dollar Cost Averaging as an Enhancement to BUY & HOLD

Definition of Dollar Cost Averaging

Dollar Cost Averaging is an investment strategy where you divide your total investment amount into smaller, equal portions and invest those amounts at regular intervals over time, regardless of the asset's price. This approach aims to reduce the impact of volatility on the overall investment by smoothing out the average purchase price.

Short Example of Dollar Cost Averaging

Scenario:

Investor: You have $1,200 that you want to invest in a cryptocurrency basket.

Dollar Cost Averaging Implementation: Instead of investing the entire $1,200 at once, you decide to invest $100 each month over the next 12 months.

Outcome: By investing regularly, you buy more units when prices are low and fewer units when prices are high, potentially lowering your average cost per unit over time.

Scenario 2:

Here is another visual example where person A is holding 1 BTC at a fixed price bought at 50K and Person B using AI Basket DCA strategy:

Person A (Lump Sum Investor):

Investment: $50,000

Strategy: Buys all at once when Bitcoin is priced at $50,000.

Result: Acquires 1 Bitcoin.

Person B (Dollar-Cost Averaging Investor):

Investment: $50,000 split into equal parts over 12 months.

Strategy: Invests periodically as Bitcoin's price declines over time.

Purchases at Prices: $50,000, $45,000, $35,000, and $25,000.

Result: Acquires more than 1 Bitcoin because they buy more when the price is lower.

Outcome Comparison:

Total Bitcoin Owned:

Person A: 1 Bitcoin.

Person B: Approximately 1.38 Bitcoins.

Average Cost per Bitcoin:

Person A: $50,000.

Person B: Lower average cost due to buying at decreasing prices.

How Dollar Cost Averaging Enhances BUY & HOLD

Dollar Cost Averaging complements the BUY & HOLD strategy by:

Reducing Timing Risk: By spreading your investments over time, you lessen the risk of entering the market at a peak price.

Promoting Discipline: Encourages consistent investing habits, reducing the influence of emotions on investment decisions.

Simplifying Allocation Management: Regular investments help maintain your desired asset allocation without requiring large sums upfront.

Implementing Dollar Cost Averaging with Asset Allocation

Choosing Initial Allocation:

Asset Selection: Determine the assets you wish to include in your basket.

Setting Target Allocations: Decide on the percentage of your investment to allocate to each asset.

Example Allocation:

Asset A: 50%

Asset B: 30%

Asset C: 20%

Implementing Dollar Cost Averaging:

Regular Investment Amounts: Decide on a fixed amount to invest at each interval (e.g., monthly).

Consistent Allocation: Each time you invest, distribute the funds according to your target allocations.

Example with Monthly Investment of $100:

Asset A: $50

Asset B: $30

Asset C: $20

Building Over Time: Your basket grows gradually, maintaining your chosen allocation percentages with each investment.

Adjusting for Market Movements

Monitoring Allocations: Market fluctuations may cause the actual value proportions of each asset to shift over time.

Example: If Asset B outperforms and increases in value, it might constitute a higher percentage of your portfolio than initially intended.

Managing Allocation Changes:

Option 1: Continue investing according to your original allocation, allowing the market to dictate changes.

Option 2: Adjust future investments to rebalance your portfolio towards your target allocations.

Example: Allocate more of your next investment to Assets A and C to offset Asset B's increased proportion.

Pros and Cons of Dollar Cost Averaging

Pros:

Mitigates Timing Risk: Reduces the risk of investing a large amount at an unfavorable time by averaging the purchase price over multiple periods.

Promotes Discipline: Encourages regular investing habits and reduces emotional reactions to market volatility.

Simplifies Investment Process: Easier to commit smaller amounts over time rather than a lump sum.

Accessible Entry Point: Allows investors with limited capital to start investing and build their portfolio gradually.

Cons:

Potential for Lower Returns in Rising Markets: If the market is consistently rising, investing a lump sum upfront may yield higher returns than Dollar Cost Averaging.

Higher Transaction Costs: Frequent investments can lead to increased fees and transaction costs.

Requires Ongoing Commitment: Necessitates regular monitoring and commitment to invest over the chosen period.

Allocation Drift: Without periodic rebalancing, your portfolio may drift away from your target allocations due to varying asset performances.

The Rebalancing Strategy with AI Basket

A preview of AI Basket preset ‘Bluechip Assets’ curated by the community

Definition and How It Differs from BUY & HOLD

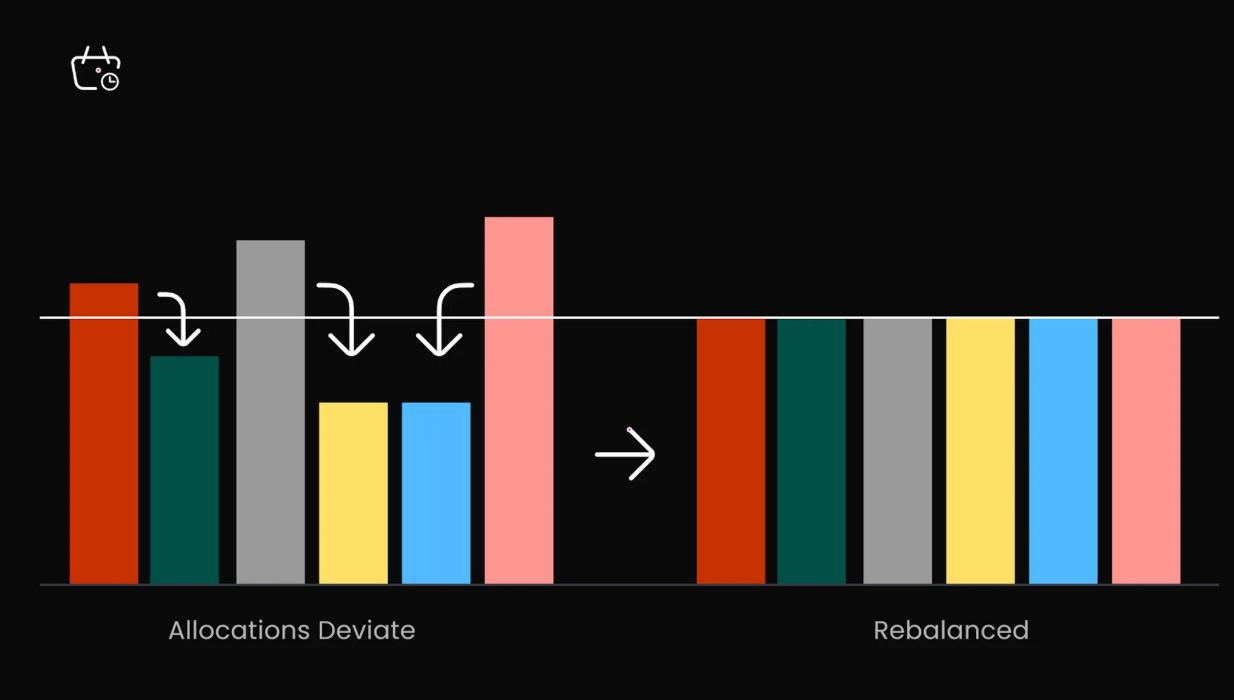

Portfolio rebalancing is a straightforward yet powerful strategy that involves periodically adjusting your basket to maintain your desired allocation of assets. This method has been a cornerstone of institutional investing for decades, with financial institutions managing billions of dollars leveraging it to mitigate risk, capitalize on market volatility, and potentially enhance returns. Unlike BUY & HOLD and Dollar-Cost Averaging, which may allow allocations to drift over time, rebalancing actively corrects these shifts.

Let's explore how rebalancing works with a practical example:

Imagine you have a cryptocurrency portfolio consisting of four assets: Bitcoin (BTC), Ethereum (ETH), Ripple (XRP), and Litecoin (LTC). Your goal is to maintain an equal allocation across these assets, so each one represents 25% of your total portfolio. If your portfolio is worth $100, you would invest $25 in each cryptocurrency.

Over time, market fluctuations cause changes in asset values:

LTC increases in value from $25 to $30.

BTC decreases in value from $25 to $20.

ETH and XRP remain at $25 each.

As a result, the composition of your portfolio shifts:

LTC now accounts for 30% of your portfolio ($30 out of $100).

BTC now makes up 20% of your portfolio ($20 out of $100).

ETH and XRP each still represent 25%.

This imbalance means your portfolio no longer aligns with your initial strategy of equal distribution.

When you rebalance an evenly distributed portfolio, you restore it to a state where each asset holds equal value.

Rebalancing the portfolio involves the following steps:

Sell a portion of the overrepresented asset: Sell $5 worth of LTC, reducing its value back to $25, so it once again represents 25% of your portfolio.

Buy more of the underrepresented asset: Use the $5 from the LTC sale to purchase additional BTC, increasing its value from $20 to $25, restoring it to 25% of your portfolio.

By making these adjustments, your portfolio returns to its original balanced state, with each asset equally weighted at 25%.

This illustration demonstrates a portfolio with a 24-hour rebalancing period. Over each 24-hour cycle, the portfolio is allowed to drift as asset values fluctuate, causing the allocation percentages to change. After 24 hours, a rebalance is performed to realign the portfolio with its desired allocations.

Rebalancing a portfolio can occur under various circumstances, but most investors opt for a periodic rebalancing strategy. This means adjustments are made at consistent time intervals. In the cryptocurrency realm, these intervals could be as frequent as every hour, day, or week. In contrast, traditional investors typically perform rebalancing on an annual basis. Traditional financial markets tend to use longer rebalancing periods like yearly because they are less volatile. However, cryptocurrency markets are far more volatile, making it feasible—and sometimes advantageous—to implement shorter rebalancing period.

How Allocation Works in Rebalancing with AI Basket

Choosing Initial Allocation:

Asset Selection and Allocation: Start by selecting assets and setting target allocation percentages, similar to BUY & HOLD and Dollar Cost Averaging.

Example: 40% Asset A, 30% Asset B, 30% Asset C.

Maintaining Allocation Over Time:

Automated Rebalancing:

Platform Automation: Our platform automatically monitors your basket and adjusts holdings to maintain your target allocations.

Rebalancing Actions: The system sells portions of overperforming assets and buys underperforming ones to realign with your targets.

Frequency of Rebalancing:

Regular Intervals: Rebalancing can occur at set intervals (e.g., weekly, monthly).

Threshold-Based: Alternatively, rebalancing can be triggered when asset allocations deviate beyond a certain percentage from targets. (will be released on SageMaster platform in upcoming release)

Example of Rebalancing in Action:

Initial Allocation: 40% Asset A, 30% Asset B, 30% Asset C.

After Market Movement: Asset B increases to 40%, Asset A decreases to 35%, Asset C decreases to 25%.

Rebalancing Action:

Sell: 5% of Asset B.

Buy: 5% more of Asset C to bring it back to 30%.

Result: Allocations return to target percentages.

Pros and Cons

Pros

Maintains Desired Allocation: Keeps your basket aligned with your original asset distribution.

Automated Risk Management: Reduces overexposure to any single asset.

Potentially Enhanced Returns: Capitalizes on market volatility by systematically buying low and selling high.

Convenience: Automation simplifies the process, requiring minimal effort.

Cons

Transaction Costs: More frequent trades can lead to increased fees.

Tax Implications: Selling assets may trigger taxable events.

Possibility of Reduced Gains: Selling high-performing assets might limit future gains if those assets continue to rise.

Less Control Over Timing: Automated rebalancing occurs based on predefined settings, not on market conditions.

Comparing Allocation Across Strategies

Initial Allocation Decision

BUY & HOLD:

One-Time Decision: Set your allocations at the beginning and let them ride.

Dollar Cost Averaging:

Consistent Allocation Over Time: Set allocations that guide each regular investment.

Rebalancing:

Active Maintenance: Set initial allocations that are maintained over time through automated adjustments.

How Allocation Changes Over Time

BUY & HOLD:

Allocation Drift: Asset proportions change based on market performance.

Dollar Cost Averaging:

Gradual Build-Up: Allocations may drift, but each new investment realigns purchases to your target percentages.

Rebalancing:

Consistent Allocation: Automated adjustments keep allocations at target levels, minimizing drift.

Effort Required to Maintain Allocation

BUY & HOLD:

Minimal Effort: No ongoing action needed; accept allocation changes.

Dollar Cost Averaging:

Moderate Effort: Requires regular investments but maintains allocation through consistent purchase distribution. However you can configure SageMaster AI Basket DCA feature to make it automated.

Rebalancing:

Low Effort Due to Automation: You can configure SageMaster AI Basket to handle adjustments, ensuring allocations remain on target with minimal input.

Combining Strategies for Optimal Allocation Management

One of the unique advantages of using Sagemaster is the flexibility it offers in managing allocations across different strategies. You can combine strategies to optimize how your allocations are set and maintained.

How to Combine Strategies on Sagemaster

Dollar Cost Averaging with Automated Rebalancing:

Regular Investments: Use Dollar Cost Averaging to build your basket over time, investing at your desired allocations.

Maintain Allocations: Enable automated rebalancing to adjust for market movements, ensuring your actual allocations stay close to your targets.

Initial Lump Sum with Rebalancing:

Immediate Market Exposure: Make a one-time investment with your chosen allocations.

Automated Maintenance: Use rebalancing to keep allocations consistent over time without additional investments.

Flexible Allocation Adjustments:

Adjust Allocations Over Time: As your goals or market perspectives change, you can modify your target allocations.

Platform Support: Sagemaster's platform allows you to update allocations easily, and the system will adjust your basket accordingly.

Benefits of Combining Strategies

Enhanced Control: Tailor your allocation strategy to fit your specific needs.

Risk Mitigation: Maintain your desired risk level through consistent allocations.

Optimized Performance: Potentially improve returns by ensuring your basket reflects your investment strategy at all times.

Convenience: Automation reduces the effort required to manage allocations effectively.

Making Your Decision

When deciding which strategy or combination of strategies to adopt, consider how you want to handle allocation in your basket.

Questions to Consider:

How Important Is Maintaining Specific Allocations to You?

High Importance: Rebalancing ensures allocations stay on target.

Moderate Importance: Dollar Cost Averaging helps maintain allocations during the build-up phase.

Low Importance: BUY & HOLD accepts that allocations will drift over time.

Do You Prefer Automation or Manual Control?

Automation: Rebalancing automates allocation maintenance.

Manual Control: BUY & HOLD requires less intervention but offers less control over allocations.

What Is Your Tolerance for Allocation Drift?

Low Tolerance: Use rebalancing to minimize drift.

High Tolerance: BUY & HOLD allows allocations to change based on market performance.

How Do You Want to Allocate Your Initial Investment?

Lump Sum: BUY & HOLD with or without rebalancing.

Gradual Investment: Dollar Cost Averaging allows you to spread out your investment over time.

Conclusion

Understanding how allocation works within each strategy helps you make more informed decisions about managing your AI Basket. Whether you prefer the simplicity of BUY & HOLD, the gradual investment approach of Dollar Cost Averaging, or the consistent allocation maintenance of Rebalancing, Sagemaster provides the tools and automation to support your chosen strategy.

Key Takeaways:

BUY & HOLD:

Set initial allocations and accept changes over time.

Simple and requires minimal ongoing effort.

Dollar Cost Averaging:

Build your basket gradually, maintaining allocations with each buy cycle.

Reduces timing risk and promotes disciplined investing.

Rebalancing:

Keep allocations consistent through automated adjustments.

Manages risk and aligns your basket with your investment strategy.

Combining Strategies:

Use Dollar Cost Averaging and Rebalancing together for gradual investment and consistent allocation.

Customize your approach to suit your goals and preferences.

Disclaimer: Trading involves significant financial risk and can result in substantial losses. Past performance does not guarantee future results. SageMaster does not provide financial advice. Users should ensure compliance with local regulations.